On September 2, the Centers for Disease Control and Prevention delivered some unexpected relief to renters across the country. Arguing that “housing stability helps protect public health” in a pandemic, the agency issued a nationwide ban on evictions for nonpayment of rent until the end of the year.

Millions of Americans are still unemployed, and the nationwide rent freeze has only bought them a few months. But as policymakers race to figure out how to deliver rental assistance and other relief to the tens of millions of families who could face eviction come January 1, they are discovering an inconvenient fact: eviction data is so bad there’s often no way to tell who is most at risk of losing their home, where they live, or how much back rent they’re likely to be evicted over.

Real-time data on which cities, counties, and neighborhoods are seeing the highest eviction rates could help municipal leaders direct rent assistance funds, lobby for additional federal and state funds for hard-hit cities and counties, and prioritize whose doors to knock on to get the word out about assistance programs. Local data on how much back rent tenants owe would allow Congress to determine with specificity the amount of assistance renters in each state would need. But nothing close to that level of data is available. The media uproar over eviction tsunamis hides an increasingly embarrassing fact: We don’t even know how many Americans were evicted in 2019. How, then, are we supposed to help the estimated 30 to 40 million renters who are at risk of being evicted in 2021, when the moratorium lifts?

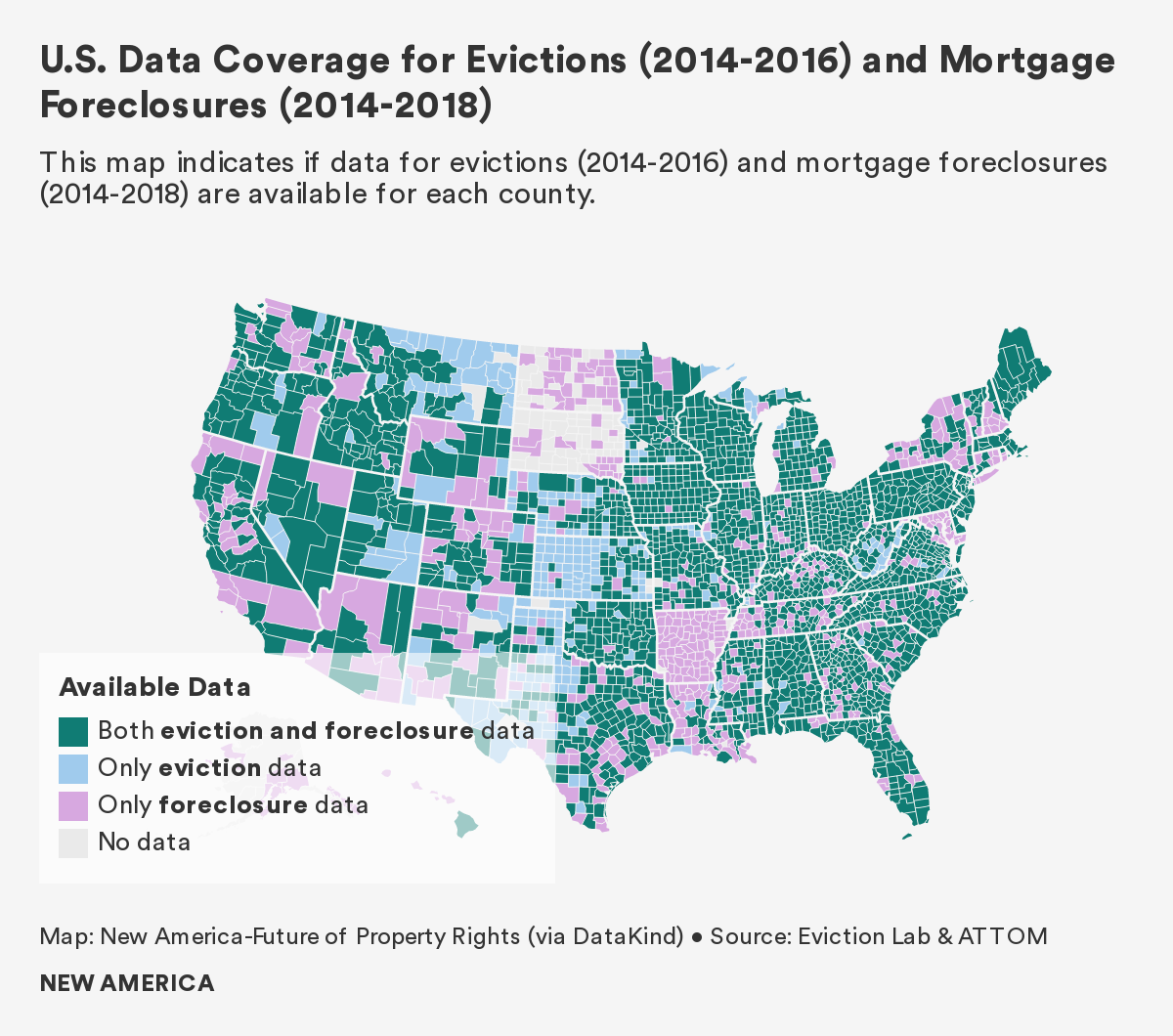

Astonishingly, foreclosure data is not any better. More than a decade after a national foreclosure crisis, there is still no public database of foreclosures. Whereas Princeton’s Eviction Lab has created a publicly available (albeit limited) national dataset on evictions, foreclosure data is largely hidden behind the paywalls of for-profit companies like Attom Data and CoreLogic. Accessing foreclosure records for a single U.S. county costs thousands of dollars per year.

Indeed, a new report from New America that I co-authored finds that one in three U.S. counties have no available data on how many people lose their homes through eviction and foreclosure each year. Without critical information about where in the county evictions and foreclosures take place, or who is most impacted, municipal leaders are flying blind as they attempt to deploy diminishing amounts of pandemic aid.

{kind=link}

Anyone who has searched for a home on Zillow or Redfin might be puzzled by the paucity of U.S. housing-loss data. How can we know the number of three-bedroom townhomes on the market in Virginia at any given moment, but not the number of people in the state who lost their homes to foreclosure?

Anyone who has been screened for an apartment might be similarly puzzled. For a small fee, any landlord can check whether a tenant has an eviction on their record. So why can’t the renter check how many tenants the landlord has ever evicted?

The answers involve mandates and money.

Consider, for one thing, how agencies collect data on homeless populations and low-income housing. Federal mandates require homeless service providers to collect and share information on homeless populations with the Department of Housing and Urban Development, and for HUD to monitor the use of Housing Choice Vouchers. But no such mandate exists for collecting data on how people lose their homes.

When it comes to money, real estate companies like Zillow, CoreLogic, ATTOM, and Black Knight comprise a lucrative industry focused on collecting granular real estate data, bundling it, and selling it to brokerages, rental sites, insurance companies, and even government agencies. But there’s no profit in providing public data on how many people have lost their homes through eviction and mortgage foreclosures. So, while some companies collect this information for commercial purposes, they have no incentive to make it accessible.

Another barrier is the decentralized land-administration process. Evictions and foreclosures are decided by more than 3,300 different courts, each of which does things a little differently. For example, as Eviction Lab explains, courts record evictions by different names. Some courts seal their eviction records. Other courts don’t digitize their rulings, relegating them to dusty binders with printed sheriff sales notices.

With no mandate to standardize or aggregate data, counties are free to decide how accessible to make it. In Forsyth County, North Carolina, for example, a single call to the county geographic information system office produced an orderly spreadsheet of all eviction records. On the other hand, a third of Maricopa County, Arizona’s eviction records were missing judgment information, the county’s foreclosure records were only available for purchase from third parties, and it took six months of pestering before the county was finally able to tell us that they had no tax foreclosure records to share.

In short, local policies, differences in institutional capacity, and a lack of standardization across jurisdictions countrywide lead to a frustrating inability to pull together housing loss data in any meaningful way.

This has serious implications. For one, without knowing how many people are losing their homes and where they live, municipal leaders can’t prioritize housing aid and outreach. Eviction Lab has built the closest proxy to a national eviction dataset, but the latest available data is from 2016 and is missing several states. Not only that, but researchers say that in some places two thirds of all evictions are informal—meaning they never go to court—and we have no way to count them. Mortgage foreclosure data is similarly patchy. Even for-profit aggregators like Attom Data have no foreclosure records for 400 U.S. counties. Tax lien foreclosure—responsible for nearly 150,000 families losing their homes in Detroit alone between 2002 and 2016—is a complete black box. No entity publicly publishes or even sells nationwide tax foreclosure data. Experts estimate that natural disasters cause more than 1 million Americans to lose their homes annually, but these rough estimates say nothing about where the housing loss occurred or what happened to the people displaced.

If we’re going to solve America’s housing-loss crisis, we have to start with fixing the data.

Without good data, we rely on anecdotal evidence and media narratives to understand housing loss. For example: in the uproar over the nation’s eviction crisis, we have lost sight of the fact that nearly 700,000 households lose their homes to mortgage foreclosure every year.

And, when data is available but not publicly accessible, it tends to fall into the hands of the wealthy and powerful, often at the expense of the vulnerable. For example, after the Great Recession, Wall Street purchased foreclosure data en masse. This allowed private equity, hedge funds, and other investors to buy hundreds of thousands of single-family homes in foreclosure, totaling over $60 billion in value, and reshape entire neighborhoods. Meanwhile local governments were unable to access those same datasets, which could have allowed them to help vulnerable homeowners hang on to their homes.

If we’re going to solve America’s housing-loss crisis, we have to start with fixing the data.

We need national eviction and foreclosure databases. Despite calls for an eviction database, most notably through Colorado Sen. Michael Bennett’s 2019 Eviction Crisis Act, no such tool has materialized, and the Federal Housing Finance Agency’s skeleton database to track homeowners who are late on their mortgages only covers 5 percent of the country.

A first step would be to standardize court data, institute digitization requirements and find a way to aggregate the data from the counties up to the states. A second critical step would be to think hard about how to provide decision-makers with the data they need while protecting the privacy of those who are losing their homes.

We also have to get better at tracking new and obscure forms of housing loss, everything from foreclosures for nonpayment of property taxes and forced sales of heirs property passed down without a will, to informal evictions and disaster-caused housing loss. It is likely that millions of people are impacted, but they are invisible to courts, researchers and aid agencies.

If nothing else, 2020 has taught us the wisdom of Peter Drucker’s famous adage: “if you can’t measure it, you can’t improve it.” Solving our nation’s eviction and housing crisis is no exception.

from Slate Magazine https://ift.tt/2S7qkJX

via IFTTT

沒有留言:

張貼留言